An exit valuation multiple is the number a buyer applies to your company’s financial metric, typically EBITDA, to determine what they will pay at the time of sale. Understanding how exit valuation multiples work is the single most important thing you can do before entering any sale process. Get the multiple wrong, and you leave millions on the table. Get it right, and you control the outcome. This article explains the mechanics, the benchmarks, the pitfalls, and the steps you can take right now to command a premium number.

How exit valuation multiples are calculated and applied

The core formula is simple: Valuation = Multiple × Financial Metric. The financial metric is usually EBITDA (earnings before interest, taxes, depreciation, and amortization), EBIT, or SDE (seller’s discretionary earnings). The multiple is a market-derived number that reflects what buyers in your industry are currently paying per dollar of that metric.

Three multiples dominate mid-market transactions:

- EV/EBITDA is the most widely used. It measures enterprise value against operating earnings and works well for capital-intensive businesses.

- EV/EBIT accounts for depreciation and amortization, making it more relevant for asset-heavy companies where those charges reflect real economic wear.

- SDE multiples apply to smaller owner-operated businesses, typically those with under $2M in revenue, where the owner’s personal compensation is added back to earnings.

The difference between a 5.5x and a 7.0x multiple on $3M EBITDA is a $4.5M valuation gap. That gap does not come from growing your earnings. It comes entirely from how buyers perceive your business’s risk and growth potential.

One adjustment that significantly affects the calculation is normalized EBITDA. Buyers will recast your financials to remove one-time expenses, owner perks, and non-recurring items. A higher normalized EBITDA raises the base, and a higher multiple raises the ceiling. Both levers matter.

Pro Tip: Always prepare a normalized EBITDA schedule before entering a sale process. Buyers will recast your numbers anyway. Doing it first puts you in control of the narrative.

Enterprise value and equity value are not the same thing. Enterprise value includes debt and excludes cash. Equity value is what you actually receive. A buyer paying 7x EBITDA on enterprise value will subtract your outstanding debt before writing your check. Know the difference before you negotiate.

What factors drive exit multiples and 2026 industry benchmarks

Exit multiples are not arbitrary. Higher multiples reflect superior growth expectations, strong return on invested capital relative to the cost of capital, and lower perceived risk. Buyers pay more when the business can grow without the owner and when cash flows are predictable.

Four factors move your multiple up or down:

- Industry sector. Buyers pay more for recurring revenue models and high-margin businesses.

- Growth trajectory. A business growing at 20% annually commands a higher multiple than one flat for three years.

- Revenue predictability. Contracted or subscription revenue reduces buyer risk and raises the multiple.

- Owner dependency. A business that runs without you is worth more than one that stops when you leave.

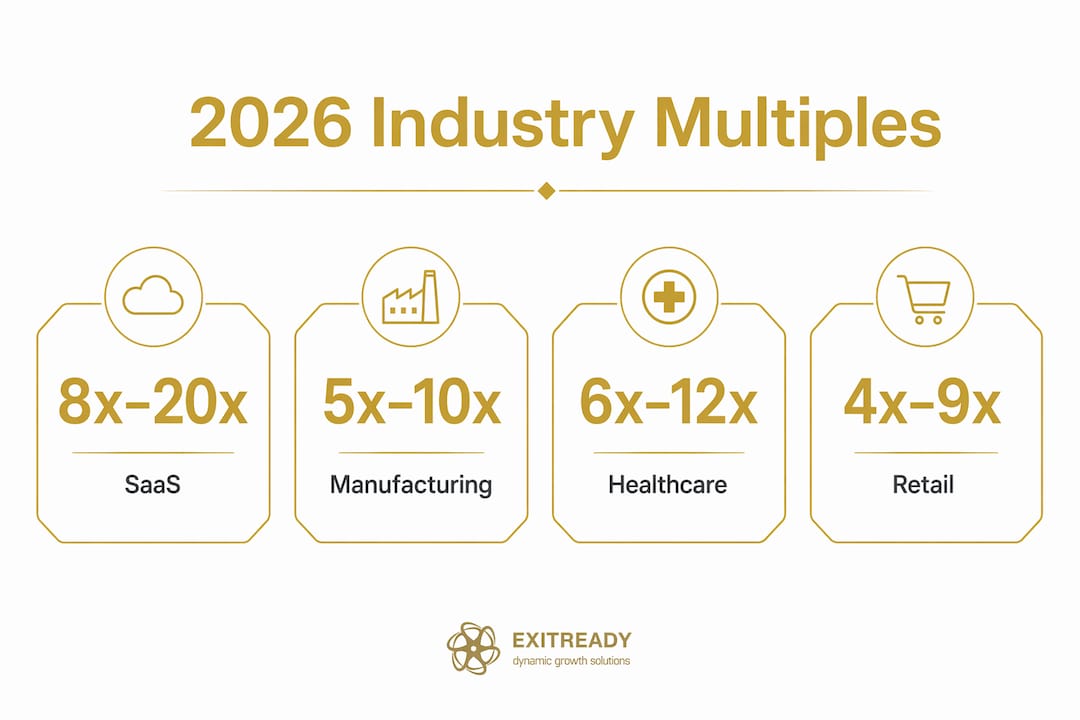

Current 2026 benchmarks show wide variation by sector. Industry multiples vary significantly based on growth profile and risk:

| Industry | EBITDA Multiple Range | Notes |

|---|---|---|

| SaaS | 8x–20x | Recurring revenue, high margins |

| Veterinary | 12x–20x | Consolidation-driven demand |

| HVAC | 5x–10x | Fragmented, acquisition-heavy |

| Manufacturing | 4x–7x | Capital-intensive, cyclical |

| Small business (SDE) | 2x–4x | Owner-operated, limited scale |

These ranges are not ceilings. A manufacturing business with documented systems, diversified customers, and consistent margins can exceed its sector average. The benchmark tells you where the floor is, not where you have to land.

Selecting the right peer group for comparison is critical. Comparing your HVAC business to a national SaaS platform produces a meaningless number. Your comparable group must match your industry, your size, your growth rate, and your risk profile.

Pro Tip: Ask your M&A advisor to show you the actual transaction comps they are using. If the peer group includes companies twice your size or in adjacent industries, push back.

Common pitfalls and misconceptions about exit multiples

The most dangerous misconception is treating your multiple as a fixed number you can look up. Multiples are pricing shorthand that compress many variables into one figure. They miss capital structure differences, interest rate environments, and business-specific risk factors.

Common mistakes owners make include:

- Anchoring to 2020–2021 multiples. Interest rates were near zero then. Higher rates today compress what buyers can pay and still hit their return targets. Comparing your expected multiple to that era sets you up for disappointment.

- Focusing only on EBITDA growth. Growing earnings matters, but structural risk factors can keep your multiple low even as EBITDA climbs. Two businesses with identical $5M EBITDA can trade at 5x and 9x based entirely on customer concentration, revenue predictability, and management depth.

- Using a single number instead of a range. Professional buyers present sensitivity tables with multiple scenarios. Anchoring your expectations to one number ignores how buyers actually model risk.

- Ignoring the peer group. Broad or outdated comparable sets produce misleading benchmarks. A peer group built on transactions from three years ago in a different rate environment is not a reliable guide.

“Multiples can be misleading if the underlying capital structure and interest rate environment are ignored. Owners who benchmark against 2020–2021 transaction data without adjusting for today’s rate environment risk overestimating their exit proceeds by a material margin.”

The practical implication is clear. Your multiple is not just a market number. It is a judgment about your business’s specific risk profile. Reduce the risk, and the multiple moves.

How exit multiples apply to terminal value and exit planning

Exit multiples play a central role in discounted cash flow (DCF) valuation, specifically in calculating terminal value. Terminal value represents the bulk of a company’s total estimated value in a DCF model. Exit multiples drive 50%–80% of that terminal value figure, which means the multiple you apply at the end of your projection period has an outsized effect on the total valuation output.

The exit multiple method works as follows:

- Project your company’s free cash flows for a defined period, typically five years.

- Apply a market-derived exit multiple to your projected EBITDA in the final year.

- Discount that terminal value back to the present using your weighted average cost of capital (WACC).

- Add the discounted terminal value to the sum of discounted cash flows from the projection period.

The result is your estimated enterprise value. A small change in the exit multiple applied in step two produces a large change in the final number. That is why the multiple deserves as much attention as the cash flow projections themselves.

Professionals validate the exit multiple method against the perpetuity growth method. A divergence greater than 25% between the two methods signals a problem with your assumptions. If the two methods produce wildly different numbers, your multiple or your growth rate is off.

| Scenario | Projected EBITDA | Exit Multiple | Terminal Value |

|---|---|---|---|

| Conservative | $4M | 5x | $20M |

| Base case | $4M | 7x | $28M |

| Optimistic | $4M | 9x | $36M |

The table above shows why buyers use multiple ranges and sensitivity tables rather than a single number. The same EBITDA produces a $16M swing in terminal value depending on the multiple applied.

To command a higher multiple at exit, focus on four structural improvements:

- Reduce owner dependency. Document your processes and build a management team that operates without you. Buyers pay a premium for businesses that do not require the seller to stay.

- Diversify your customer base. No single customer should represent more than 15% of revenue. Concentration is a multiple killer.

- Build recurring revenue. Contracts, retainers, and subscriptions reduce buyer risk and justify higher multiples.

- Clean up your financials. Three years of audited or reviewed financials with clear normalized EBITDA removes friction from due diligence and signals professionalism.

A structured exit planning process addresses all four of these areas systematically, well before you enter a sale process.

Key Takeaways

Exit multiples determine your sale price more directly than EBITDA growth alone, making multiple optimization the highest-leverage activity in any exit preparation plan.

| Point | Details |

|---|---|

| Multiple × metric = valuation | A 1.5x increase in multiple on $3M EBITDA adds $4.5M to your sale price. |

| Industry benchmarks vary widely | SaaS trades at 8x–20x EBITDA; small owner-operated businesses at 2x–4x SDE. |

| Structural risk drives the multiple | Customer concentration, owner dependency, and revenue predictability move multiples more than raw earnings growth. |

| Terminal value is multiple-sensitive | Exit multiples account for 50%–80% of DCF terminal value; a small change in multiple creates a large valuation swing. |

| Peer group precision matters | Comparing your business to the wrong set of companies produces a misleading benchmark and a flawed negotiating position. |

Why the multiple matters more than you think

Most owners I work with spend years focused on growing EBITDA. That is the right instinct, but it is only half the equation. The multiple is the other half, and it is often the more powerful one.

A business that grows EBITDA from $2M to $3M while staying at a 5x multiple adds $5M in value. The same business holding EBITDA flat at $2M but moving from 5x to 7x adds $4M. Combine both, and the effect is compounding. The owners who understand this early start working on their multiple years before they plan to sell.

The part that surprises most owners is how much structural factors outweigh financial performance in a buyer’s multiple decision. I have seen two businesses with nearly identical earnings trade at very different multiples because one had documented systems and a functioning management team while the other ran entirely through the owner. Buyers are not just buying your cash flow. They are buying their confidence that the cash flow continues after you leave.

My practical advice: get a business exit readiness assessment done at least two years before you plan to sell. Use it to identify where your multiple is being discounted. Then fix those things. The return on that work, measured in sale proceeds, is almost always the best investment you will make.

— Andre

How Dynamicgrowthsolutions prepares owners for premium exit multiples

Dynamicgrowthsolutions works with mid-market owners who want to exit at the top of their industry’s multiple range, not the bottom. The AOS (Accelerated Operating System) replaces owner dependency with documented processes, builds management depth, and creates the operational structure buyers pay a premium to acquire.

Owners who go through the AOS program address the exact structural factors that suppress multiples: customer concentration, undocumented processes, and businesses that cannot run without the founder. If you are preparing for an exit in the next two to four years, understanding what a business operating system does for your valuation is the right place to start. Dynamicgrowthsolutions also connects owners with a network of buyers, advisors, and fractional executives who understand how to position a business for a premium outcome.

FAQ

What is an exit valuation multiple?

An exit valuation multiple is a market-derived number applied to a financial metric, typically EBITDA or SDE, to estimate a company’s sale value. It reflects what buyers in a specific industry are currently willing to pay per dollar of earnings.

How do you calculate an exit multiple?

Multiply your normalized EBITDA (or chosen financial metric) by the appropriate market multiple for your industry and size. A $3M EBITDA business at a 7x multiple produces a $21M enterprise value before debt adjustments.

What EBITDA multiple is typical for a mid-market business in 2026?

Mid-market EBITDA multiples in 2026 range from 5x to 10x for most sectors, with high-growth recurring revenue businesses like SaaS reaching 8x–20x and smaller owner-operated businesses trading at 2x–4x SDE.

Why do two businesses with the same EBITDA sell at different multiples?

Structural factors like customer concentration, owner dependency, and revenue predictability cause multiples to vary widely even when earnings are identical. A business with diversified customers and documented systems commands a higher multiple than one that depends on a single customer or the owner’s daily involvement.

How can I increase my exit multiple before selling?

Reduce owner dependency by documenting processes, diversify your customer base so no single client exceeds 15% of revenue, build recurring or contracted revenue, and present three years of clean, normalized financials. Each of these changes reduces buyer risk and justifies a higher multiple.